Artificial intelligence (AI) has entered a new phase in accounting.

After several years of experimentation, AI is becoming part of everyday finance operations. Nearly every accounting software platform now offers AI-powered features, assistants, or autonomous agents designed to help teams close the books faster, investigate exceptions, prepare journal entries, and automate repetitive work.

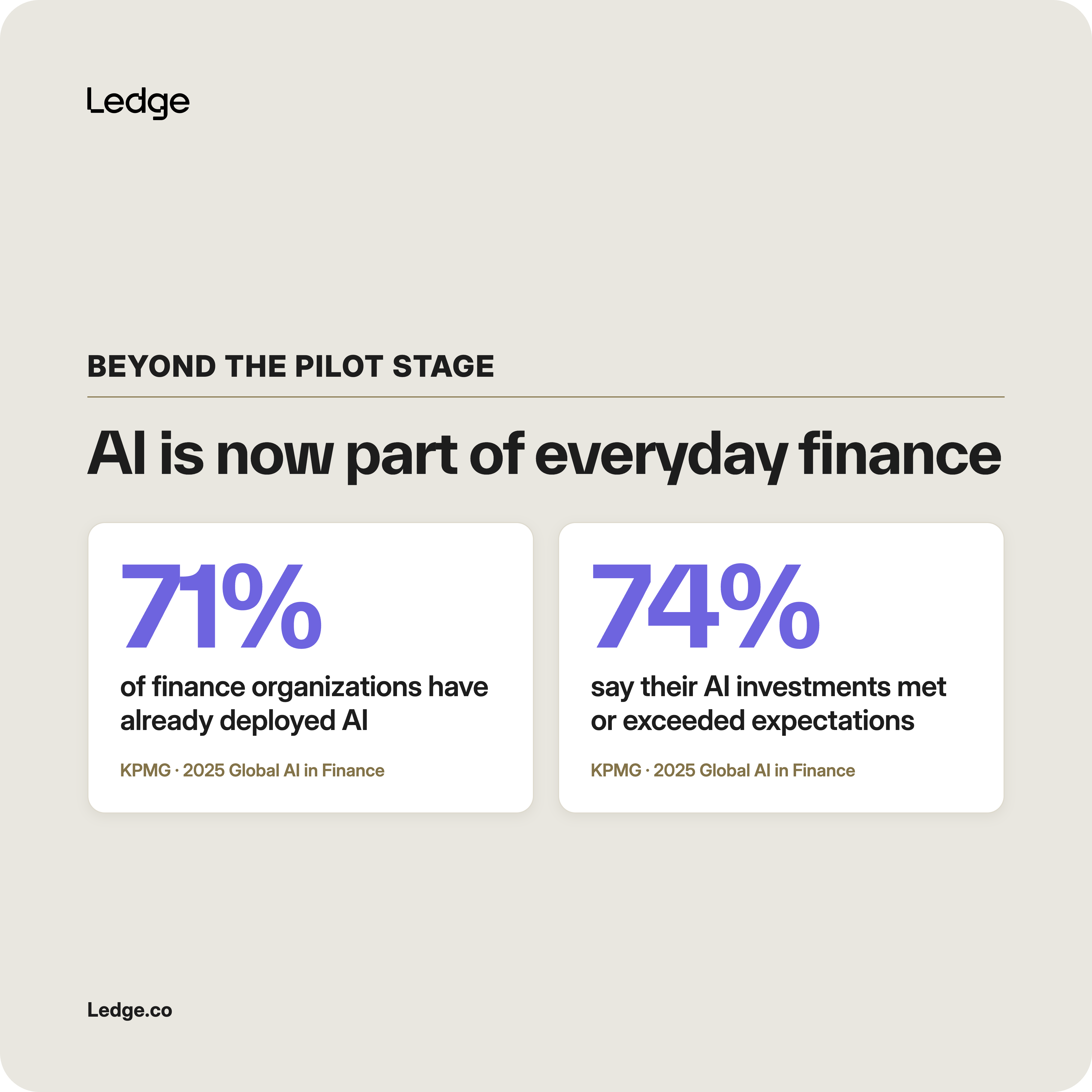

Finance organizations are adopting these tools quickly. According to KPMG's 2025 Global AI in Finance survey, 71% of organizations worldwide have already deployed AI within their finance function. Among organizations that have implemented AI, 74% say their AI investments have met or exceeded expectations.

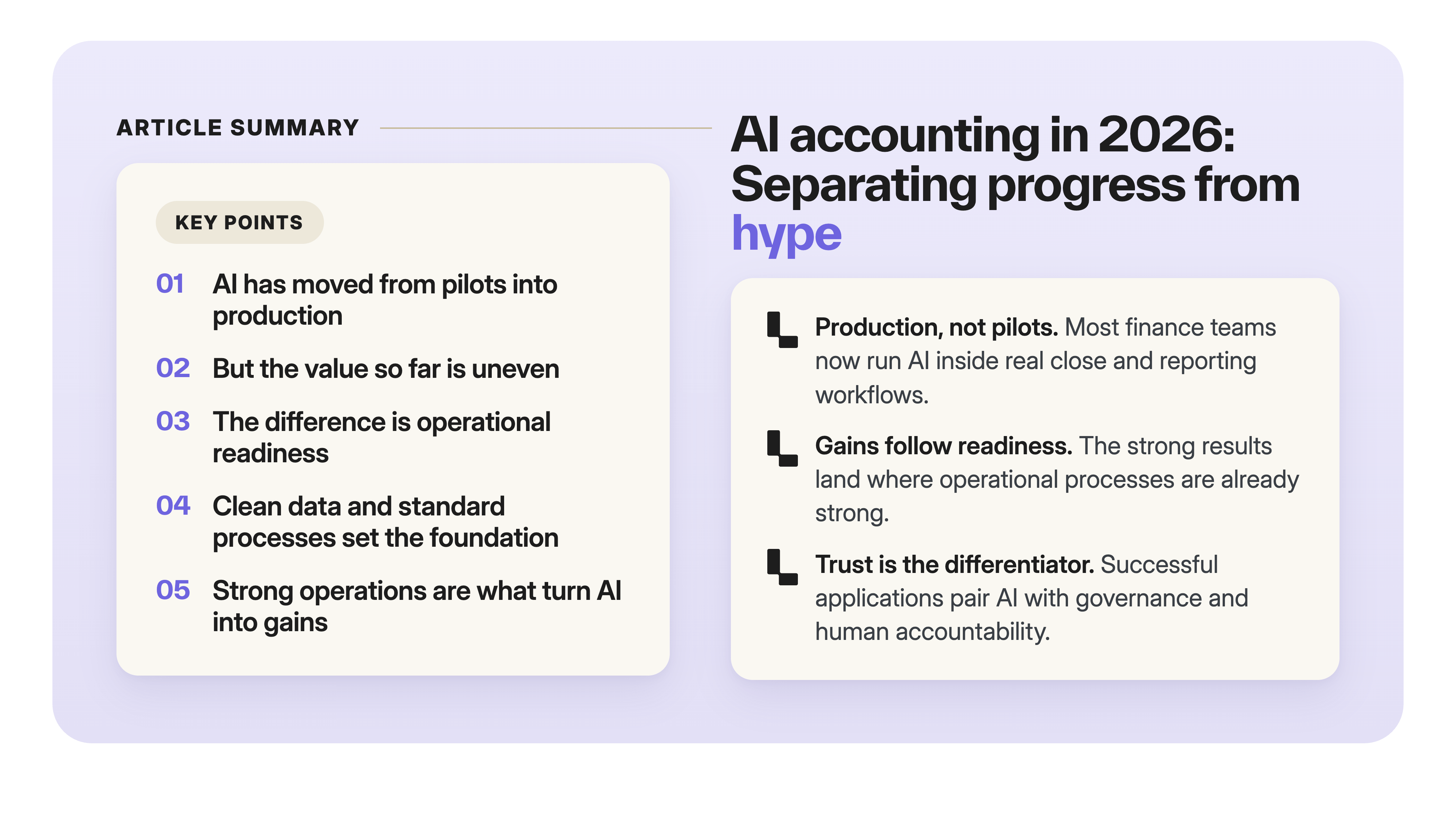

Those numbers suggest AI has moved well beyond the pilot stage. But they do not tell the whole story.

The bigger story is that accounting has become one of the first enterprise functions where AI must consistently perform in a high-stakes, highly controlled environment.

Unlike many business applications, accounting demands more than useful outputs. Every financial decision must be supported by evidence. Every journal entry must be reviewed. Every reconciliation must withstand anaudit. Success depends not only on what AI can produce, but on whether finance teams can understand, verify, and trust its work.

This is why accounting has become such an important proving ground for enterprise AI. The question is no longer whether large language models can summarize documents or answer questions. It is whether they can operate reliably inside the financial control environment that organizations have spent decades building.

The evidence so far paints a nuanced picture. AI is already creating measurable value in areas such as reconciliations, financial research, journal entry preparation, and close management. At the same time, many organizations continue to struggle with governance, process maturity, data quality, and scaling AI beyond individual use cases.

This report examines that reality by separating measurable progress from marketing claims. Rather than asking what AI could do, it explores what AI is actually doing in accounting today—and what finance leaders should watch as the profession enters its next stage of transformation.

What is the landscape of AI adoption in accounting today?

Before asking whether AI is transforming accounting, it's worth understanding where the profession stands today.

The first thing that becomes apparent when examining the data is that AI has moved well beyond experimentation. Finance organizations are no longer asking whether AI belongs in accounting—they are actively deploying it across their operations. At the same time, the data suggests the profession has entered a more challenging phase: scaling AI responsibly and demonstrating measurable business value.

The numbers below illustrate how quickly the landscape is evolving.

AI is becoming part of everyday accounting operations

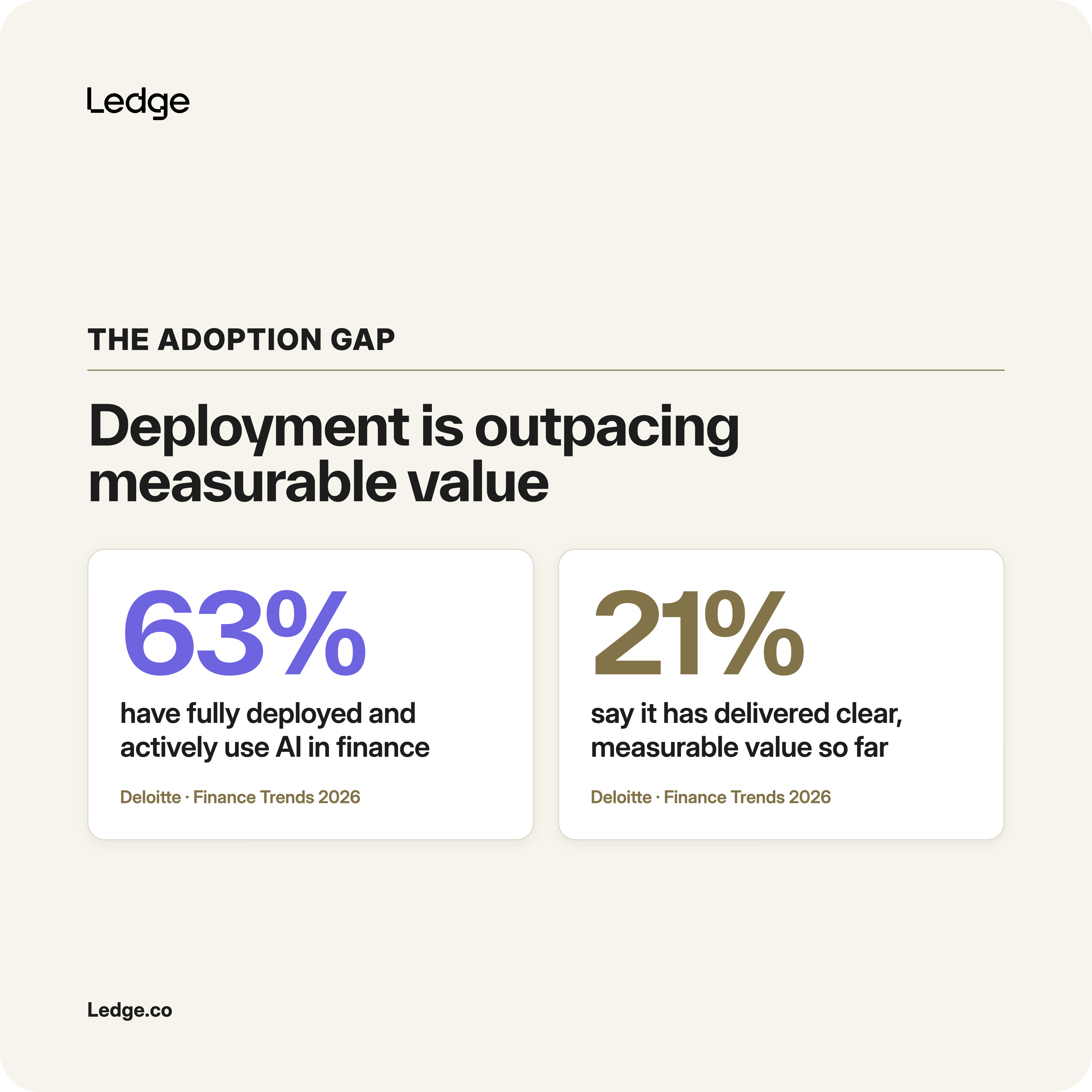

According to Deloitte's Finance Trends 2026 survey, 63% of finance departments report that they have fully deployed and actively use AI solutions within the finance function. Yet only 21% say those investments have delivered clear, measurable value to date, suggesting that implementation is outpacing realized business impact

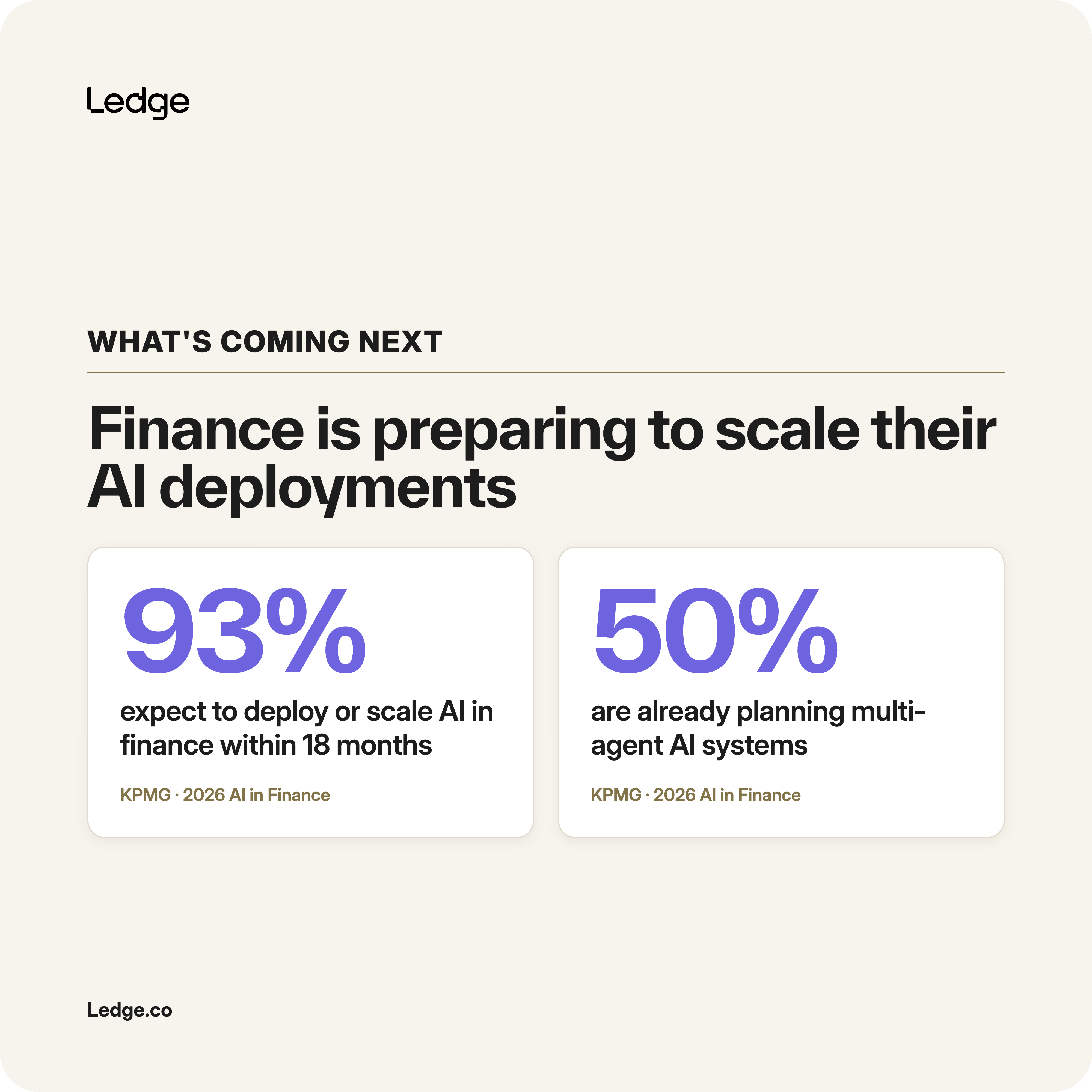

Finance leaders are preparing to scale AI

KPMG's 2026 AI in Finance report found that 93% of U.S. companies expect to deploy or scale AI within their finance functions over the next 18 months.

Nearly half are already planning multi-agent AI systems capable of coordinating multiple accounting and finance workflows, reflecting growing confidence that AI will become part of core finance operations rather than remain a standalone productivity tool.

Scaling AI remains the industry's biggest challenge

Deloitte found that while AI deployment has become widespread, only 14% of finance organizations have fully integrated AI agents into finance workflows.

Legacy technology, difficulty demonstrating ROI, and data privacy concerns remain among the most commonly cited barriers to scaling AI successfully.

Operational readiness is becoming the differentiator

KPMG reports that 74% of finance leaders say their AI initiatives have met or exceeded return-on-investment expectations. At the same time, the research suggests that organizations realizing the greatest value have invested not only in AI technology, but also in the governance, workforce skills, and implementation capabilities needed to deploy it effectively.

Where is AI creating measurable value for accountants?

The evidence suggests that AI is not transforming every part of accounting equally.

Instead, measurable value is beginning to emerge in a relatively small number of accounting workflows where work is repetitive, well documented, and supported by structured financial data. Across recent research, five areas appear consistently.

Financial planning and analysis

Finance leaders report some of the strongest gains in financial planning and analysis.

According to KPMG's 2026 AI in Finance report, 71% of finance leaders say AI has improved the speed of decision-making, 70% report improvements in decision quality, and 64% say forecasting accuracy has improved. Rather than replacing financial analysis, AI is helping teams synthesize information, identify trends, and prepare insights more quickly.

Financial reporting and controllership

Deloitte's Finance Trends 2026 survey identifies controllership and financial reporting among the finance functions where leaders expect AI to deliver the greatest impact.

Organizations are increasingly using AI to prepare supporting documentation, review financial information, summarize account activity, and assist with recurring reporting tasks while maintaining established review and approval processes.

Accounting research and documentation

AI is also beginning to improve knowledge-intensive work in accounting. Rather than manually searching through accounting standards, internal policies, contracts, or prior-period workpapers, finance professionals are using generative AI to retrieve relevant information, summarize technical guidance, explain accounting treatments, and accelerate research.

This aligns with guidance from the AICPA & CIMA, which notes that generative AI can enhance accounting research and analysis by helping professionals quickly locate and synthesize authoritative information. The organization emphasizes that AI should augment, not replace, professional judgment, with accountants remaining responsible for validating conclusions before they are applied to financial reporting.

As accounting standards continue to evolve and organizations accumulate larger volumes of internal documentation, AI is increasingly becoming a tool for navigating institutional knowledge rather than simply automating routine tasks.

Reconciliations and exception management

Reconciliations have long been a focus of finance automation, and generative AI is expanding those capabilities. Rather than simply matching transactions, AI can help investigate unmatched items, retrieve supporting documentation, summarize potential causes of exceptions, and organize information for accountant review.

Professional accounting guidance increasingly frames these activities as examples of AI augmenting, rather than replacing, accounting work. AICPA & CIMA notes that AI is most valuable when it helps finance professionals locate relevant information, synthesize evidence, and accelerate analysis while preserving human review and professional judgment. Similarly, CPA.com describes AI as a tool for improving efficiency across accounting workflows rather than automating professional decision-making.

In practice, this means AI is increasingly being used to reduce the time spent investigating routine discrepancies while accountants remain responsible for evaluating exceptions, determining materiality, and approving financial outcomes.

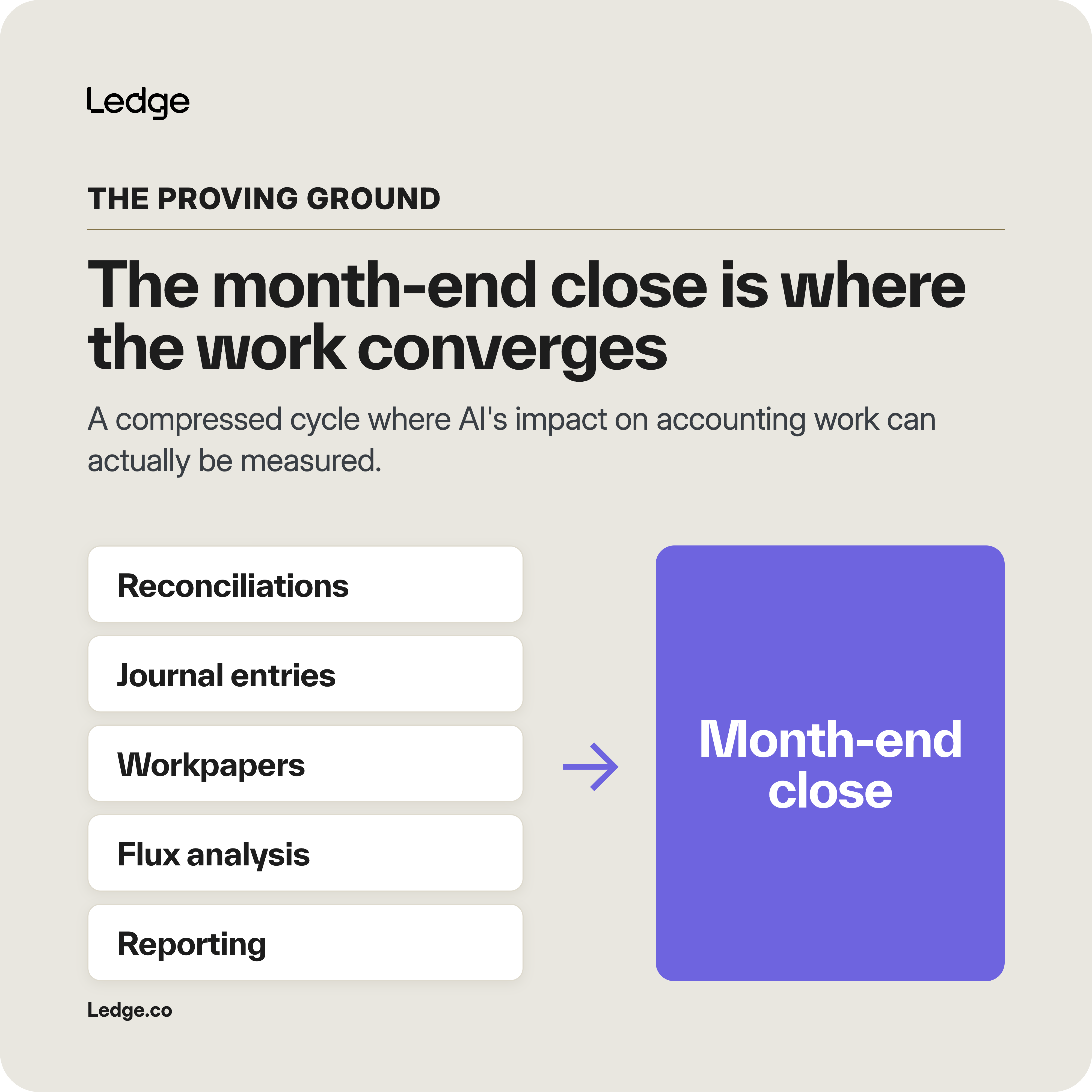

The month-end close

Many of the accounting workflows where AI is beginning to create measurable value converge during the month-end close. Reconciliations, journal entries, supporting documentation, flux analysis, and financial reporting all come together during a compressed reporting cycle, making the close a practical environment for evaluating AI's impact on accounting work.

One of the first large empirical studies of generative AI in accounting conducted by researchers from Stanford and MIT provides early evidence of these benefits. Researchers analyzed transaction-level data from 79 small- and medium-sized enterprises using AI-enabled accounting software alongside survey responses from 277 accountants. The study found that greater AI adoption was associated with an 18% increase in weekly client support, a 9% shift in accountant time away from routine data entry and toward higher-value work, a 12% increase in ledger granularity, and a 7.5-day reduction in monthly close time. These findings suggest that AI can improve both productivity and aspects of financial reporting quality when integrated into accounting workflows.

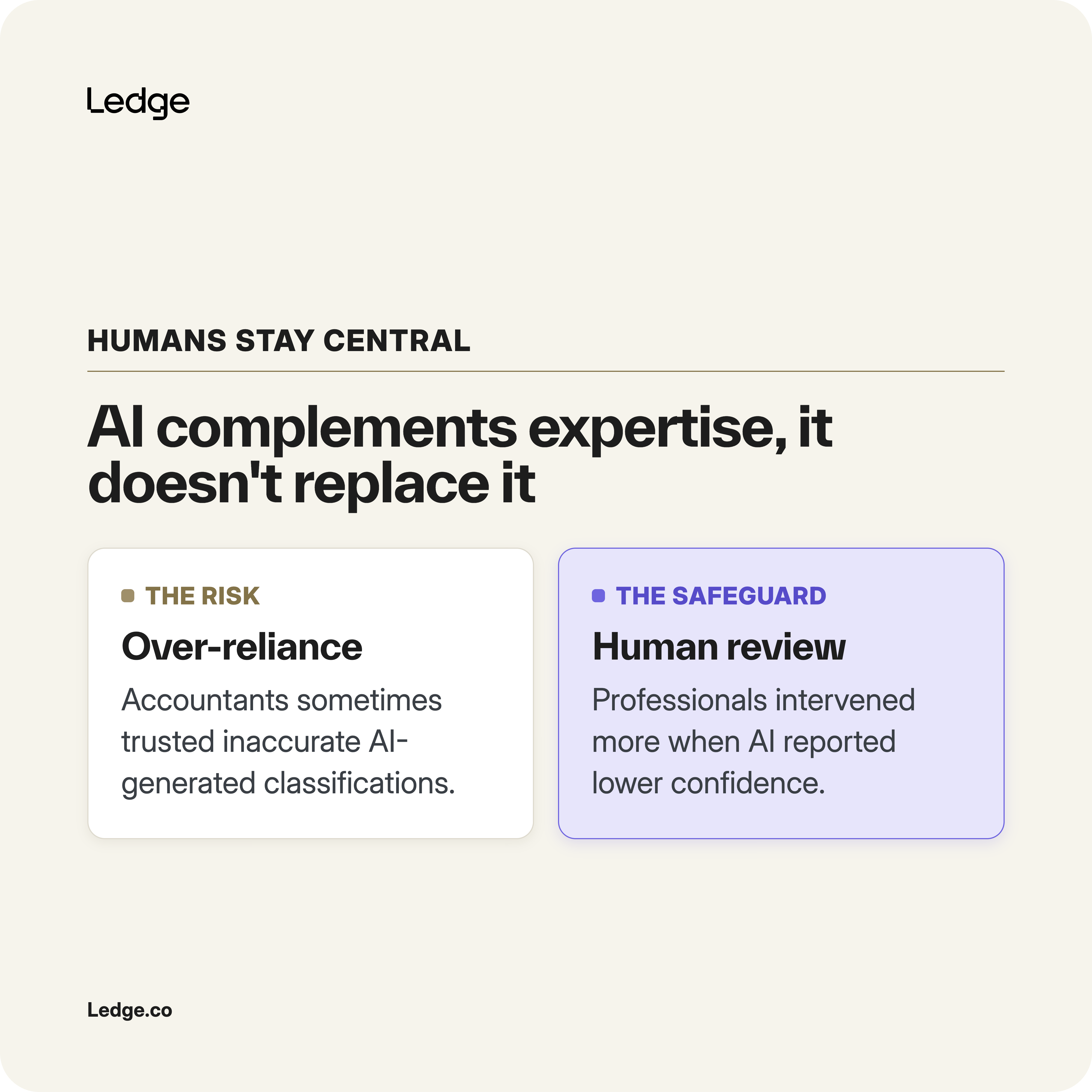

Importantly, the study also found that experienced accountants continued to play a critical role. Professionals were more likely to intervene when AI systems reported lower confidence, indicating that AI functioned as a complement to accounting expertise rather than a replacement for it. At the same time, the researchers found evidence that accountants sometimes over-relied on inaccurate AI-generated classifications, highlighting the importance of maintaining human review and appropriate controls.

Taken together, these findings reinforce a broader pattern emerging across the profession. Organizations are not replacing the month-end close with autonomous AI. Instead, they are integrating AI into individual activities throughout the reporting cycle to reduce manual effort, improve efficiency, and allow accountants to focus more of their time on analysis, review, and professional judgment.

Building an AI-ready accounting function

Across the studies referenced in this report, a consistent pattern emerges: organizations realizing the greatest value from AI are also investing in the underlying processes, governance, and operational capabilities that allow AI to be deployed effectively.

In other words, AI is amplifying the quality of existing accounting operations rather than replacing them.

Strong accounting processes remain the foundation

Many of the accounting workflows benefiting from AI today already share important characteristics. They are well documented, supported by structured financial data, governed by established policies, and subject to consistent review procedures.

These operational foundations make it easier for AI to retrieve relevant information, prepare work, and support decision-making without compromising financial controls.

Conversely, organizations with fragmented processes, inconsistent documentation, or poorly defined workflows often struggle to realize the same benefits because AI inherits many of the limitations of the underlying accounting environment.

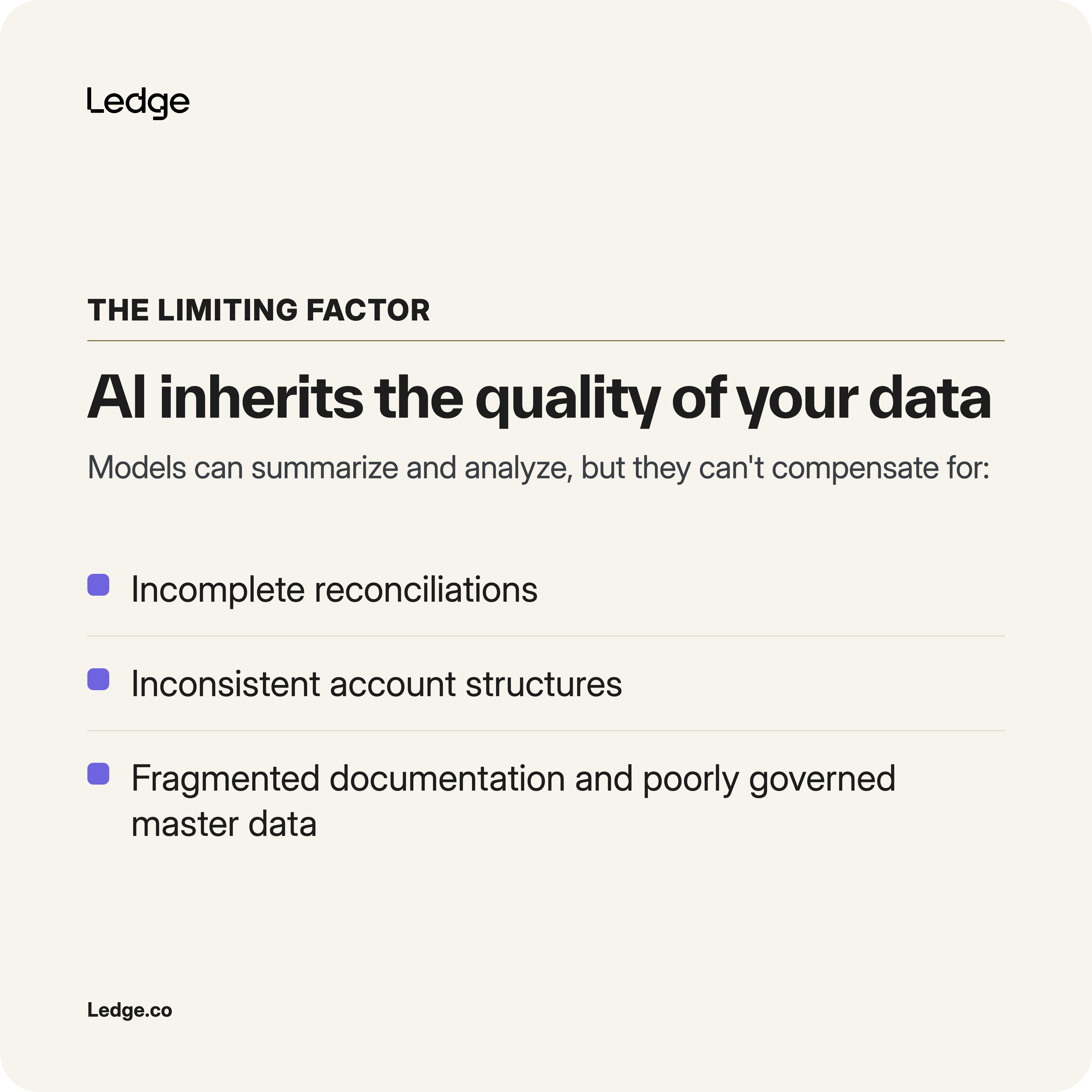

Data quality is becoming a limiting factor

One of the most consistent themes across recent finance research is that AI performance depends heavily on the quality of the underlying financial data.

Large language models can summarize information, identify patterns, and generate analyses, but they cannot compensate for incomplete reconciliations, inconsistent account structures, fragmented documentation, or poorly governed master data. As organizations expand AI across finance, investments in data quality, standardized processes, and financial governance are becoming increasingly important determinants of success.

Deloitte's Finance Trends 2026 survey similarly identifies legacy technology and data challenges among the primary barriers preventing finance organizations from scaling AI successfully. Rather than model capability, operational readiness is increasingly becoming the constraint.

Governance is becoming a clear systems-building advantage

As AI becomes embedded in financial reporting, governance is becoming increasingly important.

KPMG's 2026 AI in Finance report found that organizations with stronger AI governance and assurance capabilities reported better business outcomes than those focused primarily on technology deployment. The research suggests that organizations are increasingly differentiating themselves through implementation discipline—including clear accountability, workforce training, documentation standards, and oversight—rather than model capability alone.

This reflects a broader shift across enterprise AI. Competitive advantage is becoming less about access to AI models and more about the ability to deploy them responsibly within existing operating environments.

AI is changing the role of the accountant

As AI takes on more routine accounting work, the role of finance professionals is beginning to evolve.

The greatest productivity gains are emerging in activities such as information retrieval, documentation, reconciliations, variance analysis, and research—tasks that have traditionally consumed significant amounts of accountant time. Early evidence suggests that these efficiencies allow finance teams to shift their attention toward higher-value work, including interpreting financial results, investigating exceptions, advising business leaders, and strengthening financial controls.

For finance leaders, this suggests that preparing for AI is not simply a technology initiative. It also requires rethinking how accounting teams are organized, how work is distributed, and where professional expertise creates the greatest value.

AI rewards operational maturity

Taken together, these findings point to an important conclusion.

The organizations realizing the greatest value from AI are not necessarily those deploying the most sophisticated technology. They are often the ones with standardized accounting processes, well-governed financial data, documented policies, and disciplined review procedures.

As AI capabilities continue to improve, these operational foundations are likely to become even more important. For finance leaders, preparing for AI is increasingly becoming less about selecting the right software and more about building an accounting function that is ready to support it.

The real story of AI in accounting

Organizations are using AI to improve financial planning and analysis, accelerate accounting research, support reconciliations, streamline financial reporting, and reduce manual effort during the month-end close. Early empirical research also suggests that these applications can improve productivity, increase the quality of financial records, and shorten reporting cycles when implemented effectively.

At the same time, the research offers a more measured perspective than many industry headlines.

The greatest gains are not coming from fully autonomous accounting functions or AI systems replacing finance professionals. Instead, they are emerging from targeted applications that support existing accounting workflows while preserving governance, auditability, and professional oversight. Organizations realizing the strongest results are pairing AI with standardized processes, high-quality financial data, disciplined governance, and experienced finance teams.

Accounting has become one of the first enterprise functions where AI must consistently operate within a highly controlled environment. The organizations that succeed will not necessarily be those with access to the most advanced models. They will be those that build accounting operations capable of using those models with the transparency, discipline, and trust that financial reporting demands.