The only thing that grinds my gears more than someone calling themselves a “Polymath” is a company calling their GMV “Revenue”.

Shower thought: If a Polymath is a Vegan, what do they tell you about first?

Back to our regularly scheduled programming…

Public service announcement: GMV is not Revenue!

GMV is commonly used for marketplaces (Etsy), eCommerce businesses (Shopify), and payment gateways (Stripe) that charge a fee or take rate.

GMV is not a true reflection of a company's revenues, but rather its throughput, as most of the revenue goes to the original seller.

In other words, GMV is representative of the total order value, while Revenue is only a portion of GMV.

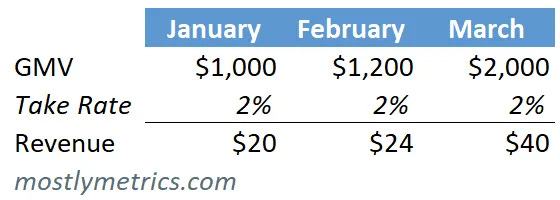

Example:

- Etsy sells a quilt on behalf of an artist for $1,000.

- Etsy takes a 2% commission.

- $980 goes to the quilt maker

- $20 goes to Etsy as net revenue

- Etsy still gets to show the full $1,000 as GMV passing through its books

But Revenue ≠ GMV!

Net Revenue, as you can see in the example above, is what the company ultimately recognizes as revenue, post supplier payouts.

For all you Quants out there, we can flip the equation:

Net Revenue = GMV * Take Rate

Net Revenue is what valuation will be based on (or should be based on). It’s difficult to value marketplaces using a multiple of GMV, since it varies depending on take rate from biz to biz.

GMV without margin = empty calories

The problem with using GMV as a north star metric is it doesn’t tell you what’s actually available to run the business.

Instead, you should be focusing on Net Revenue, Gross Margin, and (GASP) Free Cash Flow.

So whenever you are looking at any of the business models listed below, take the extra step to get to Net Revenue before making any firm valuation conclusions:

- Platform (Patreon)

- Marketplace (Airbnb)

- Aggregator (Kayak)

- Drop ship ecommerce (that fake entrepreneur you went to high school with)

- Channel-led hardware sales (Dell Technologies)

- Channel-led software sales (Rubrik)

The Valuation Rope-a-dope

Startup land is littered with examples of marketplace and ecommerce businesses that were initially valued based on a multiple of their GMV, and the metric was unfortunately prioritized from there on out.

Why did it happen? Well, it’s better than nothing when it’s still too early to judge businesses on the basis of other, more substantive metrics (like revenue, gross margin, or profitability). And this makes sense - up to a certain point.

It’s very common for a marketplace to subsidize at least one side of the market to build enough liquidity for transactions to take place. Uber did that early on - paying drivers to wait on standby so when someone finally called for a ride, they’d be able to quickly connect the two sides.

GMV, in many ways, is a leading indicator of market pull - something investors look for to detect if there are signs of Product Market Fit.

But at the end of the day, my dog would starve if I fed him GMV. He needs Net Revenue to survive.

FlipKart serves as a cautionary tale. The Indian ecommerce business peppered customers with deep discounts, subsidizing transactions from their thiccc balance sheet. It was great for media headlines. And fundraising. And employee morale. Until it wasn’t. Because it wasn’t indicative of durable revenue growth.

As soon as funding dried up, the discounts were non-sensical. It was the proverbial house built upon sand.

Another Indian startup, Snapdeal, wrote a story following a similar plot. Both the operators and the investors were mesmerized by the larger-than-life GMV topline.

After realizing they were off course, Snapdeal co-founders Bahl and Rohit Bansal wrote an email to their team admitting the mistakes they made in running the company.

“Let’s remember—GMV is vanity, profit is sanity” -Snapdeal co founders email

And as funding dried up in 2016, aggressive discounts became impossible for Snapdeal, and GMV slowed to a crawl.

In each case, GMV was a double edge sword - it initially propped up valuations, but sent management chasing its tail until it all came falling down…

But perhaps the most egregious offender of GMV was (and still is) eBay.

Sellers have long questioned how eBay determines Gross Merchandise Volume (GMV) when reporting quarterly earnings to our overlords at the SEC (Securities and Exchange Commission). In 2021, eBay shined some light on its methodology, and kinda-sorta promised to be better.

In a press release on its Investor Relations website, poetically titled, "eBay Announces Change to Gross Merchandise Volume Definition and Releases Updated Historical Metrics," the company revealed figures that gave us a peak under the hood. The way eBay calculated GMV was creating some sizeable differences:

In fact, in the fourth quarter of 2020, it added up to a $3.5 billion difference.

Back of the envelope math would say ‘mis-statements’ amounted to a 10% - 15% delta in what they ‘claimed’ as sales, that were not actually sales. And that’s just one quarter over the past +20 YEARS!

"Previously, eBay reported GMV regardless of whether the buyer and seller actually consummated the transaction," it wrote.

WTF?

Going forward, they said they would report only paid transactions. But old habits die hard. Apparently, eBay still includes shipping and taxes in its GMV figure (which I think is total crap).

Taming the chaos

There’s a lot of noise in between gross revenue and net revenue, especially when you are an ecommerce, fintech, or marketplace business with thousands of transactions applied at varying take rates.

I know because I’ve dealt with it, correction, almost died from it. You have a tangled web of ERP, invoicing solutions, payment processors, banks, ecommerce platform, and a janky homegrown database… mapped kinda like this:

This is a problem that happens slowly, and then all at once. If it’s happening to you, I strongly recommend you check out Ledge, which can help you tame your fragmented payment infra so you don’t die from continuous multi way reconciliation. Afterall, the cost of losing visibility into your revenue is sky high.

Feed your dog

What’s the lesson in all of this?

Feed your dog, and your startup, so neither die due to a crappy GMV diet.

GMV is tasty, but high in calories and low in nutritional value.

I do think GMV can be relied upon as a leading indicator and a supplemental metric. But it cannot be put on a pedestal without context, and should by no means be used as an input for valuation.

So what’s for dinner tonight?

Hopefully, it’s net revenue…

This post originally appeared on mostlymetrics.com